Hispanic Retirement Outlook Gets Worse

One thing really stood out in a recent study: the deterioration in Hispanics’ retirement prospects since the 2008-2009 recession.

Workers’ success at saving for retirement is becoming increasingly important to their financial security in old age. This puts Hispanic households at a clear disadvantage: they earn half as much as white households, which makes it that much more challenging to build retirement wealth by buying a house or saving more in their 401(k)s – two-thirds of Hispanic workers don’t even participate in an employer 401(k).

Workers’ success at saving for retirement is becoming increasingly important to their financial security in old age. This puts Hispanic households at a clear disadvantage: they earn half as much as white households, which makes it that much more challenging to build retirement wealth by buying a house or saving more in their 401(k)s – two-thirds of Hispanic workers don’t even participate in an employer 401(k).

White Americans aren’t exactly in great shape either. Today,

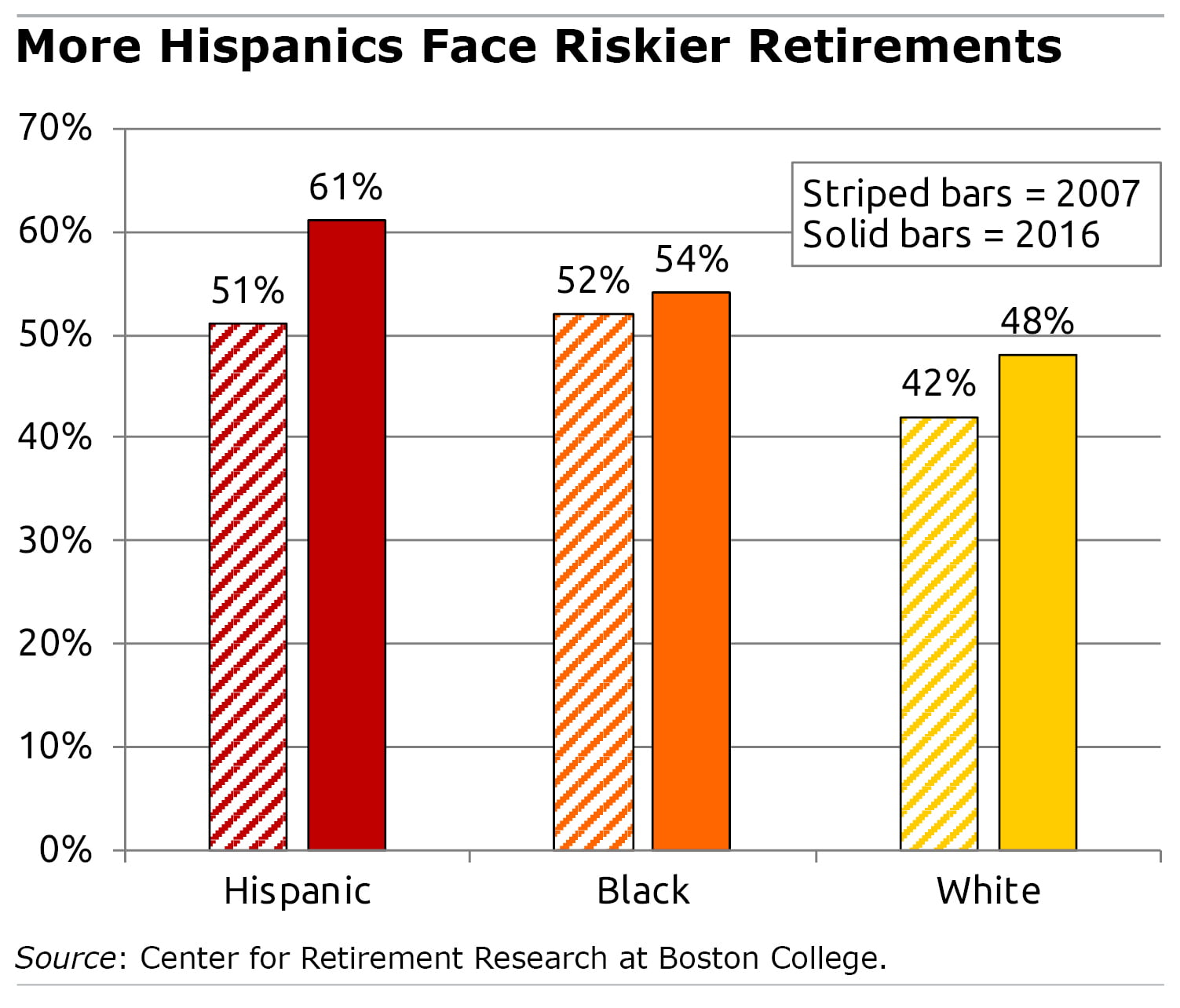

48 percent of them are at risk of experiencing a drop in their standard of living after they retire – this is 6 percentage points higher than before the recession, according to a new study by the Center for Retirement Research. Black Americans are worse off than whites, though their situation hasn’t changed much over the past decade.

But 61 percent of Hispanic workers are at risk – a 10-point jump since the recession – the study found. A big reason is that Hispanic homeowners were hit especially hard by plunging house prices during the mortgage crisis in states like Florida, Nevada, Arizona, and California, where they are heavily concentrated. Their home equity values dropped 41 percent, a result of buying “houses in the wrong place at the wrong time,” the researchers said.

The loss of home equity has a big impact on retirees by reducing the amount they can extract from their properties by purchasing less expensive housing or taking out a reverse mortgage. (The researchers assume that when workers retire, they will use reverse mortgages.)

It’s important to note here that the study was based on Federal Reserve survey data for 2016, and the economy, the housing market, and the stock market have all improved since then.

Black Americans didn’t escape the recession either. Their unemployment rate spiked to 17 percent, and the median earnings of the lowest-income blacks sank 39 percent. Oddly, these economic jolts partly explain why they saw only a 2-point increase in their retirement risk, to 54 percent, since the recession.

Low-income workers will have more modest requirements for their retirement income in the future, and Social Security acts as a buffer. The program’s progressive benefit formula replaces a higher percentage of low-income workers’ earnings.

The study’s strongest conclusion concerned Hispanic workers, who “face a much greater chance of being unable to maintain even their lower” living standards after they retire.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

Comments are closed.

Why do the researchers assume that when workers retire, they will use reverse mortgages? I could understand if the assumption is that workers can use reverse mortgages. But to assume that workers will use reverse mortgages may be a flawed assumption. Many financial advisors would say that reverse mortgages should only be used as a last resort, when all other saving vehicles have been exhausted.

That’s such a good question. The answer is a bit of paradox.

You’re absolutely right that a tiny percentage of retirees ever take out a reverse mortgage to extract some of their home equity – they don’t even like to downsize to cheaper housing.

But home equity is, nevertheless, a form of wealth, so it’s also hard for economists to ignore it when talking about someone’s financial condition.

Thanks for reading our blog!

Kim

Since NRRI seeks to identify households that may be at risk of having inadequate income in retirement, all potential sources of income are considered. It’s more methodology that assumption.

“Black Americans didn’t escape the recession either. Their unemployment rate spiked to 17 percent, and the median earnings of the lowest-income blacks sank 39 percent. Oddly, these economic jolts partly explain why they saw only a 2-point increase in their retirement risk, to 54 percent, since the recession.

Low-income workers will have more modest requirements for their retirement income in the future, and Social Security acts as a buffer. The program’s progressive benefit formula replaces a higher percentage of low-income workers’ earnings.”

Is the second paragraph meant as the explanation for the first paragraph? If not, I am confused by the “partly explained” part, as unemployment to 17% and income down by 39%, sure seems like it would increase anyone’s retirement risk by > 2%.

Thanks. Interesting article. Sad, but interesting.

Bill, thanks for keeping me honest!

You’re right that the second paragraph isn’t clear. What it means is that low-income workers living at a certain standard of living will need relatively less retirement income, too, if they’re to maintain the living standard they had when they were working.

On top of that, Social Security is a progressive program that helps low-income workers more – another support to their standard of living.

I hope this answers your question.

Kim (blogger)

Thanks for your interesting article, I would appreciate your comments to the following questions:

– I believe that many Hispanics are low-income workers and the progressive nature of Social Security benefits would have buffered their retirement benefits as well, but the immigrant nature of many Latinos and their broken pattern of employment makes their earnings records in Social Security much shorter. Is there a significant difference between the length of careers in Black Americans and Hispanics to account for this disparity? Or is it something else?

– Hispanics where targeted with sub-prime loans even when many of them qualified for prime rates. So, there is no surprise in the findings of the study related to the impact of the mortgage crisis among Hispanic homeowners. What surprises me is the researchers’ finding that it was a result of buying “houses in the wrong place at the wrong time”. I believe it has more to do with the types of credit they were offered. Can you elaborate on how location played a part?

– Considering the recovery side of the equation one issue that disproportionally affects White Americans positively is that many of them have retirement accounts that invest, to a large extent, in equities. When capital markets recovered, so did retirement accounts of many Americans. Conversely, most Hispanics lack retirement accounts, and those that have them tend to invest more conservatively, so improvements in the equity markets since the recession did not produce the same wealth effect. Did the study consider the differences in asset allocation by race in their projections? Is there any recommendation on how to improve on this?