Explaining Social Security’s Earnings Test

The reduction in benefits for some people who collect Social Security while simultaneously working is frequently called a “tax.”

It is not a tax. Under a Social Security rule known as the Retirement Earnings Test (RET), some benefits are withheld if the worker earns above a certain level – $19,560 in 2022 – and has not yet reached his full retirement age under the program. At that age, the government starts paying the deferred benefits back incrementally.

As older workers plot a path to retirement, they should have a clear understanding of this financial impact. But a new study finds they have a poor grasp of the tradeoff that is the central feature of the RET: a smaller monthly check now, while they’re working, in return for a bigger check later.

Failing to understand this concept has real world consequences. Retirement experts encourage boomers to work as much as possible to improve their finances. But someone who doesn’t understand the RET might decide against working more to prevent a perceived benefit cut.

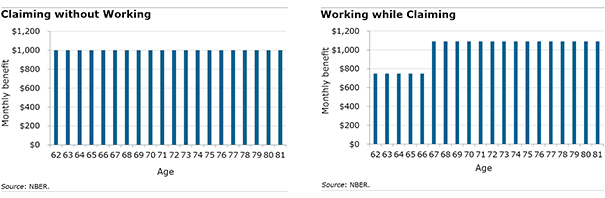

The researchers experimented with how to improve understanding of the RET by showing some 1,000 older workers numerous graphic representations of the financial impact. The best way to illustrate the study’s main finding – that a bar chart emphasizing the shift in benefits from now to later worked best – is to focus here on two pairs of blue bar graphs.

Some workers saw a simple bar graph (below, left) showing that the individual who fully retired at age 62 would receive a $1,000 monthly benefit for life. A second bar graph (below, right) showed a smaller benefit – about $750 per month – for someone who started Social Security at 62 while he was still working. At 67, his full retirement age, the benefit jumps to about $1,100 when Social Security starts paying back the withheld amount. A second group of workers also saw the simple bar graph (above, left) of the 62-year-old retirees’ stable $1,000 benefit. But the second bar graph (below) illustrated the shift in benefits for a Social Security recipient who is still working.

A second group of workers also saw the simple bar graph (above, left) of the 62-year-old retirees’ stable $1,000 benefit. But the second bar graph (below) illustrated the shift in benefits for a Social Security recipient who is still working.![]() Between 62 and 67, the blue bars for $750 benefits are capped by lightly shaded bars representing the withheld amount. At 67, the benefits jump to almost $1,100 – and the amount of the increase is shaded in gray on the bars.

Between 62 and 67, the blue bars for $750 benefits are capped by lightly shaded bars representing the withheld amount. At 67, the benefits jump to almost $1,100 – and the amount of the increase is shaded in gray on the bars.

To test how well the various graphs had worked, the researchers then asked questions about a hypothetical worker. The shaded graph showing the shift in benefits due to the RET was more effective than simply showing the jump in benefits at the full retirement age.

For example, the group who saw the graph depicting the shift absorbed one important concept behind the RET – that is, they were significantly more likely to correctly answer that someone who claims at 62 but continues working, resulting in a smaller monthly benefit during the early years, will end up receiving roughly the same total benefits over his lifetime as the person who had started Social Security and fully retired at 62.

Understanding the impact of the RET “is crucial to helping [workers] make more informed decisions about how much to continue working,” the researchers said.

To read this study, authored by Megan Weber, Stephen Spiller, Suzanne Shu, and Hal Hershfield, see “Communicating the Implications of How Long to Work and When to Claim Social Security Benefits.”

The research reported herein was derived in whole or in part from research activities performed pursuant to a grant from the U.S. Social Security Administration (SSA) funded as part of the Retirement and Disability Research Consortium. The opinions and conclusions expressed are solely those of the authors and do not represent the opinions or policy of SSA, any agency of the federal government, or Boston College. Neither the United States Government nor any agency thereof, nor any of their employees, make any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of the contents of this report. Reference herein to any specific commercial product, process or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute or imply endorsement, recommendation or favoring by the United States Government or any agency thereof.

Comments are closed.

One note not mentioned in this article is that since 2000 SS recipients have lost between 30 to 35% in buying power due to inflation; that means additional sources of income are required to keep up with inflation.

Thank you for the update on this.

So you get the same amount over your lifetime working or not? So why work?

Because, for many people, Social Security alone is not enough to live on, so people have to continue to work and save to make ends meet.

My wife retired in 2001 and will turn 70 early next year. Is it worth delaying the benefit application for 7 months?

Dear Carmelo- That’s a decision that only you and your wife can make. But try this:

Create an account on Social Security’s website and look up her benefits. Go to My Social Security (or Google this: My Social Security account).

You’ll need her Social Security number to create an account so you can look at her benefits.

Scroll down and you will see a chart. Just slide the bar to look at her monthly benefits now (69 and 5 months) and in 2023.

Good luck!