COVID-19 Could Increase US Inequality

A growing number of Americans can’t pay their rent, and the queues forming outside food banks hint at human need on the scale of the Depression. For Americans who were already living paycheck to paycheck prior to the pandemic, the $1,200 relief checks the government has deposited into their bank accounts are too little and came too late.

Few are being spared the financial fallout from the COVID-19 economic contraction. But economists predict the damage being done to working and middle class people will cause another surge in U.S. inequality, just as the previous recession did.

The big unknown is whether this downturn, which is unfolding more violently than the previous one, will do even more damage to livelihoods and produce an even bigger increase in inequality. Some economists say the unemployment rate is approaching 20 percent – double the peak reached in 2009.

New York University’s Edward N. Wolff, who has studied inequality for decades, predicts wealth inequality will spike again within the next two years. In the last recession, wealthy people lost money in the stock market, but the middle class did much worse.

The typical U.S. household’s net worth – their assets minus their debts – plunged by 44 percent between 2007 and 2010. This ended a 15-year period of stability relative to wealthier households, pushing inequality to historic highs.

The vulnerability in middle America’s finances back then remains a vulnerability today: debt. The Federal Reserve Bank of New York was already reporting early signs of growing financial distress among credit card borrowers prior to the current contraction, and Wolff said that the ratio of debt to net worth in the middle class is currently higher than it is for other groups. This debt, when combined with a fall in investment portfolios and an expected decline in house prices, will push up wealth inequality, he said.

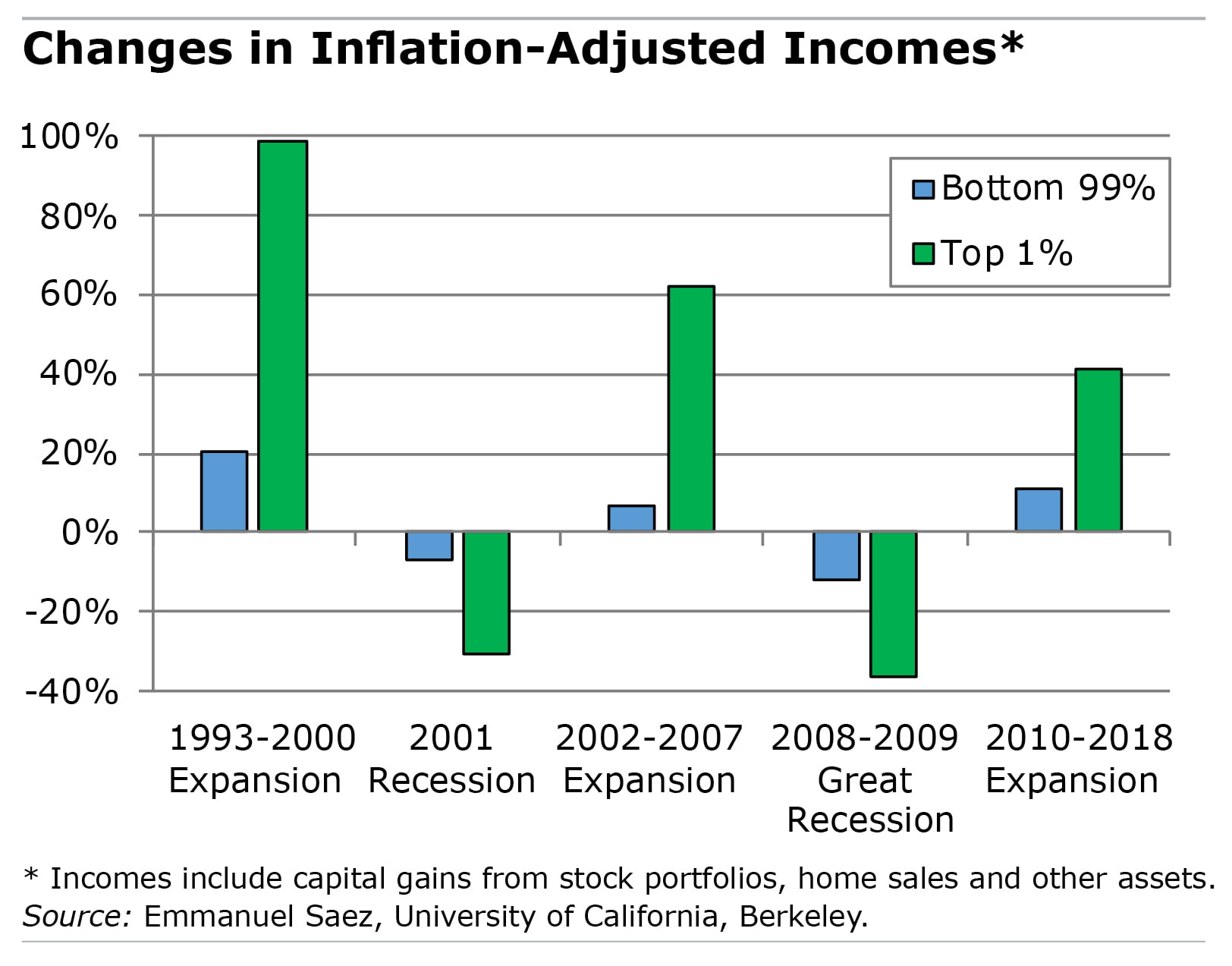

Another form of inequality – the disparity in incomes – widened after the last recession and Boston College economist Geoffrey Sanzenbacher worries that it will increase again. Between 2008 and 2018, the top 1 percent of U.S. families received nearly half of the increase in incomes for all U.S. families, adjusted for inflation.

Another form of inequality – the disparity in incomes – widened after the last recession and Boston College economist Geoffrey Sanzenbacher worries that it will increase again. Between 2008 and 2018, the top 1 percent of U.S. families received nearly half of the increase in incomes for all U.S. families, adjusted for inflation.

Sanzenbacher, who writes a blog about inequality, said that what distinguishes the current downturn from the 2008 recession explains why income inequality could go up this time around.

After the 2008 financial crisis, millions of the Americans who lost their jobs were relatively well-paid professionals in finance and business services who could scrape together enough money to weather the downturn. Of course, lower-income workers were laid off too. But the current contraction has hit lower-paid service workers first and hardest in industries like travel, restaurants and retail.

They often work for small businesses, which employ half of all U.S. workers. As the country pulls out of the coronavirus shutdown, “my biggest fear is that small employers don’t make it,” Sanzenbacher said.

The workers in these industries, who are disproportionately women, minorities, and immigrants, are the least able to handle losing their wages.

Read more blog posts in our ongoing coverage of COVID-19.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

Comments are closed.

I’ve never liked the word inequality used in this context. Of course there’s inequality. There are people who are smarter than me and who work harder than me, and they deserve to be wealthier than me. The problem is with continuing concentration of wealth, what Anand Giridharadas calls a “winners take all” economy. If I recall correctly, there was a top 0.1% in 1980 who enjoyed a well-deserved status and a pretty good life, but their relative wealth was not as great as it is today. In any event, the problem isn’t with there being winners. It’s with the taking all. It just isn’t sustainable.

Inequality is only getting worse in the US over the past 30 years. In fact the US has one of the the largest wealth gaps of any country in the world; the 1% own 40% of all the wealth in the US; they hold over 25 Trillion in wealth; top 10% in US own 70% of the nation’s wealth. Laws passed by congress help the wealthy avoid taxes such as: capital gains tax rate and carry forward interest. The highest 20% income represented 1/2 of all US income in 2018; if this continues to accelerate at present rate do not be surprised if there is not a revolution in the US just like The French revolution in their early history. When average Americans can not house nor feed their families they have NOTHING to lose.

Relief is skewed to larger employers, who get favorable access to loans. Many southern states are opening up early mostly to be able to refuse unemployment benefits to low wage (often black) workers since their jobs are available even if unsafe. The low wage health workers such as home health aides and nursing home staff are at very high risk, but cannot “work from home,” and are usually forced to use public transportation. Government of the rich, by the rich and for the rich. We have got to change.

It really baffles me why most pundits seem to think that inequality is all about these economic crashes that we have experienced in 2008 and now in 2020. Real median income in 1986 was about $55K in 1986 and is now about $64K as per the federal government. I wish the issue of inequality would be discussed in more realistic terms. This is a structural issue that is continually ignored by most people.

https://fred.stlouisfed.org/series/MEHOINUSA672N

This is not a surprise; we talk about it all the time:

– it takes money to make money (as the old saying goes)

– we know which occupations pay good wages;

– we know what qualifications provide access to those occupations;

– we know the “success sequence” of how to get there;

– and we know how to grow wealth

Success results by making these right decisions early so as not to derail opportunities. Otherwise, even the basics will be out of reach.

A second point is that this is not a zero-sum game. It’s not the wealthy against the non-wealthy. Just because you make a million dollars doesn’t mean that I can’t. Just because someone else is rich doesn’t mean that you and I can’t be. There isn’t a finite amount of wealth or income out there. Anyone can get theirs. The pie simply grows larger for however many do.

It’s up to each of us to adapt to the times and make the right choices to get us where we want to be.