Array of Financial Products is Dizzying

Rather than put his money in a bank, my cousin, who’s in his mid-40s, makes loans in $25 increments on a peer-to-peer lending website. He decides on the amount of risk he’s willing to take on – and the riskier the borrowers he chooses, the more he earns on his “savings.”

Rather than put his money in a bank, my cousin, who’s in his mid-40s, makes loans in $25 increments on a peer-to-peer lending website. He decides on the amount of risk he’s willing to take on – and the riskier the borrowers he chooses, the more he earns on his “savings.”

My cousin’s $25 investments illustrate how much our consumer finance market has evolved over several decades. We all embrace the convenience. Car loans are a more affordable way to buy a vehicle, Internet banking lets homebuyers get several mortgage quotes at once, and paying with cell phones is much easier than paying with cash or even credit cards.

But all this innovation has a downside. One example is the change from installment credit with fixed payments in the early 1960s to revolving credit, which lets consumers choose to pay a small required minimum – and increases the high credit-card interest that undisciplined borrowers pay. A recent and egregious innovation is companies that purchased lawsuit settlements from victims of lead paint poisoning for a fraction of their value. Both innovations offer convenience in exchange for personal financial impacts that are either excessive or difficult to recognize.

A primary outcome of all this financial innovation is that U.S. households “in aggregate have taken on greater risk,” conclude professors at the Harvard Business School in their 2010 paper, “A Brief Postwar History of US Consumer Finance.” Consumers now have an enormous amount of latitude – arguably too much latitude – to borrow, shift assets, save for retirement (or not), play the markets, or engage in peer-to-peer lending, they say.

As a result, risks pervade our investment portfolios, savings and retirement accounts, borrowing decisions, and how we purchase consumer goods. And that’s the problem.

“As Americans have been given more options, and have been asked to make their own financial decisions,” the authors conclude, “they are apparently ill equipped to make choices that foster household financial health.”

They trace the increased risk to two things that characterize personal financial and credit products: a proliferation of the choices available to financial consumers and the rise of do-it-yourself financial products.

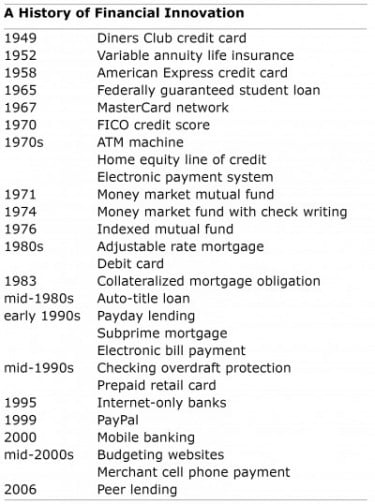

Choice in financial and credit markets, as illustrated in the timeline of financial innovations accompanying this article, has increased steadily since 1949. That’s when a Manhattan businessman conceived the Diners Club credit card for travel and entertainment expenses after he forgot to bring his wallet to a restaurant. Innovations expanding choice have, for example, encouraged households to move their savings out of federally insured certificates of deposits at traditional banks to stock market mutual funds or sometimes to day-trading accounts. Electronic debit and credit cards and ATMs, while convenient, carry overdraft fees, late fees, and other charges for people who aren’t diligent about their finances.

The growth of DIY financial products has also increased the responsibility that falls on consumers’ shoulders. A major example is the complex task of investing and drawing down retirement plan assets that this blog often writes about. Others include managing home equity lines of credit and online brokerage accounts.

The authors connect the decline in household savings rates and increase in leverage with consumers’ eagerness to embrace financial innovation. Household debt, as a percentage of personal income, has grown six-fold between 1946 and 2008. Mortgages are a good reason for this, but while they’ve transformed homeownership, the proliferating options have included subprime home loans for buyers who might not have qualified for traditional mortgages with tougher approval processes.

Financial innovations have been beneficial in many ways – reducing mortgage interest rates, enhancing returns on savings, and providing less costly financial transactions. But there’s an important lesson for consumers as we go about our daily financial affairs: think before you innovate!

To stay current on our Squared Away blog, we invite you to join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here.

Comments are closed.

Oh, for heaven’s sake, you’ve proved me wrong again! All those times I’ve blamed Sears & Roebuck for starting this mess. Their little numbered disks that were hung on the wall introduced the “little guy” to unsecured debt so I thought that was the genesis of all of this. You guys are just too smart – now we can blame lots of folks. Figure 3 in the report stops at 2008 and shows ratio improvements. It would interesting to know if that was a lesson learned or just a anomaly not seen since.

I enjoy reading your blog a lot. However, your conclusion that correlation is causation seems to be a very shallow conclusion to make. The principle reason for the increase in personal debt and fall in saving is the rise in inequality levels. Since the mid 70s, adjusted for inflation, wages have risen very little. Also, there are many millions of Americans who are without a banking relationship or who are under-banked.

You forgot to mention that on the budgeting side we now have tools to keep track of and plan our spending that are much better and easier to use. I refer to spreadsheets, online tracking tools at financial institutions, and products like Intuit Quicken, MS Money, and similar online tools, such as Mint. It wasn’t until the 1970s that pocket calculators were affordable.

This is a good article, but I would like to read something on saving money vs earning money.