Reducing Poverty for Our Oldest Retirees

With more Americans today living into their 80s and beyond, the elderly are becoming more vulnerable to slipping into poverty.

To reduce the poverty risk facing the oldest retirees, some policy experts have proposed increasing Social Security benefits for everyone at age 85. Under one common proposal analyzed by the Center for Retirement Research in a new report, the current benefit at this age would increase by

5 percent.

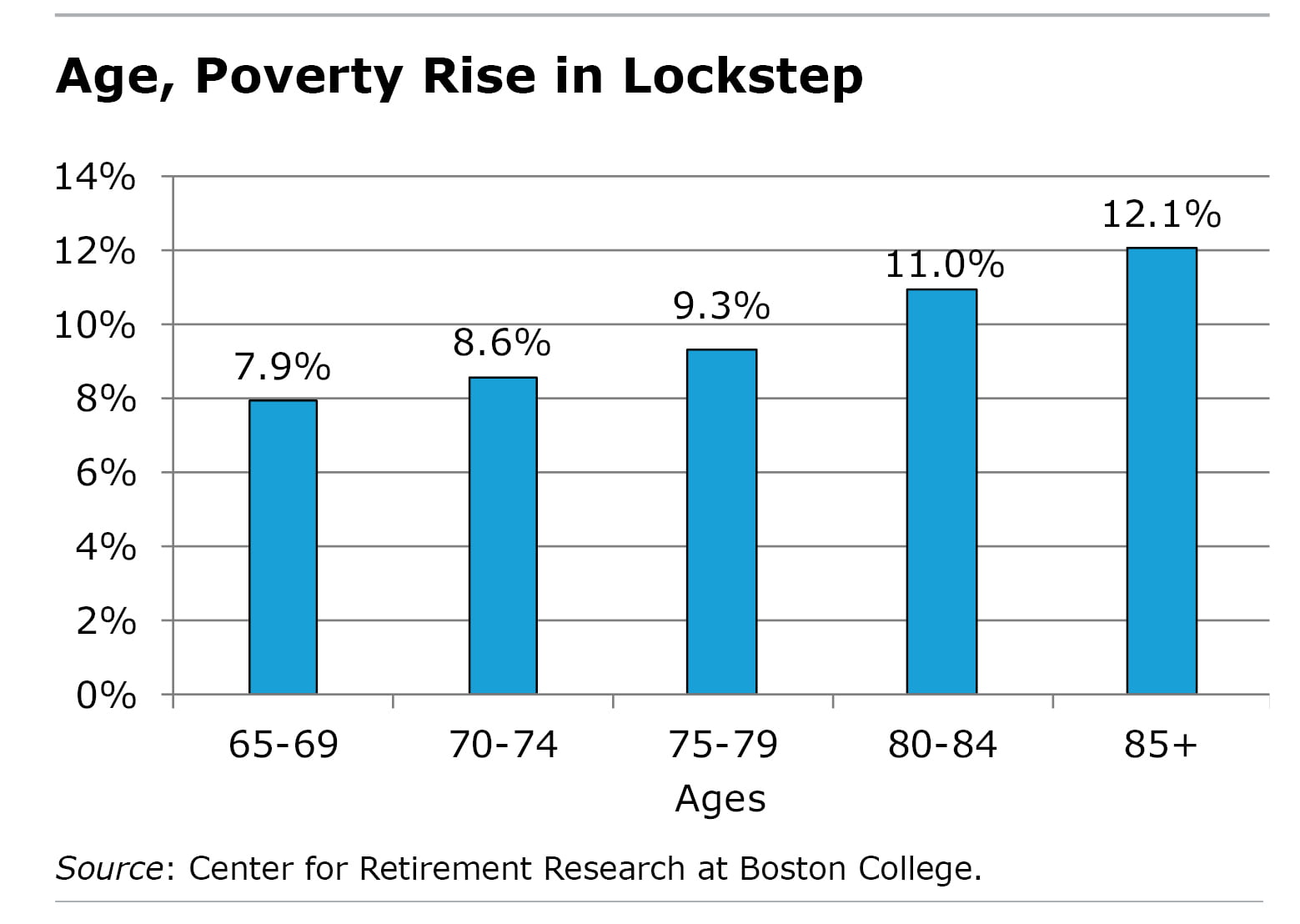

The poverty rate for people over 85 is 12 percent, compared with 8 percent for new retirees. But more elderly people may actually be living on the edge, because the income levels that define poverty for them are so low: less than $11,757 for a single person and less than $14,817 for couples.

One reason the oldest retirees are especially vulnerable is that their medical expenses are rising as their health is deteriorating, yet they’re too old to defray the expense by working. This is occurring at the same time that the value of their employer pensions – if they have one – has been severely eroded by inflation after many years of retirement.

One reason the oldest retirees are especially vulnerable is that their medical expenses are rising as their health is deteriorating, yet they’re too old to defray the expense by working. This is occurring at the same time that the value of their employer pensions – if they have one – has been severely eroded by inflation after many years of retirement.

Further, elderly women are more likely to be poor than men, because wives usually outlive their husbands, which triggers a big drop in income that is generally not fully offset by a drop in their expenses.

Limiting the 5 percent benefit increase to the oldest retirees would ease poverty while containing the cost. One way to pay for this would be to slightly reduce Social Security’s annual cost-of-living adjustment, or COLA. Cutting the COLA from, say, 2.00 percent to 1.94 percent would redirect resources away from the years when a retiree is younger and generally better off to the later years when her risk of becoming poor increases.

A variation of this proposal would increase benefits for all 85-year-olds by the same dollar amount – rather than a percentage. Both options would cost about the same, but the dollar increase would have the advantage of giving a larger boost in benefits to the lowest-income elderly people.

The researchers conclude that a flat-dollar increase “is the best way to target those most at risk” – and this could be done at relatively little cost to the Social Security program.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here. This blog is supported by the Center for Retirement Research at Boston College.

Comments are closed.

As usual, this problem is almost always about personal choices, and there are easy fixes, especially for the elderly women.

There are many life insurance and other financial products available, whereby individuals could solve this poverty problem without government intervention.

My father passed away early, but Mom did well afterwards due to his military pension, civil service pension, and social security benefits. Many retirees I know find themselves in similar circumstances.

The government doesn’t always need to step in to solve our problems when we can easily solve them ourselves.

Brian – please re-read your own comment. Your mother did well because of your father’s military pension and his civil service pension and Social Security. These are ALL government benefits! This is akin to saying “government, hands off my Medicare.” Very few of my elderly patients had the luck to get that trifecta, and the oldest old, particularly women, were barely scraping buy. A revenue-neutral way to get more to those with greatest need sounds like a great idea.

For more on the health problems of the elderly, see my book, Prescription for Bankruptcy.

Brian – please re-read your own comment. Your mother did well because of your father’s military pension and his civil service pension and Social Security. These are ALL government benefits! This is akin to saying “government, hands off my Medicare.” Very few of my elderly patients had the luck to get that trifecta, and the oldest old, particularly women, were barely scraping buy. A revenue-neutral way to get more to those with greatest need sounds like a great idea.

For more on the health problems of the elderly, see my book, Prescription for Bankruptcy.

Those are all examples of employment-based jobs & related benefits – choices that anyone can make – no different than my choice of employment in the private sector with similar benefits. It’s all about personal choices affecting our later years.

Most all of my mother’s widowed friends had two if not all three of those pension sources.

None of those (military, civil service, etc. or private sector employment choices for that matter) is – as the article’s SS example promotes – requesting the government to “step up” a benefit for a particular class of people when they, on their own, could have done this themselves by making better choices. It incentivizes bad decisionmaking.

When does it end? Personal choices determine outcome. Choose well.

There is no revenue-neutral way to do this, as recent discussions regarding reducing the SS COLA demonstrated. It will simply pile on more taxes.

Brian, Agree with you on the cost. The first thing the Government must do is shore up existing benefits before you compound the issue.

Brian, You cannot push you own family’s personal experiences on to the general public. You have no idea what anyone else’s circumstances are and to generalize the situation is, frankly, rather selfish and short-sighted. School teachers are one glaring example in which there are very few who can live outside the poverty level, not only while working but more so in retirement, despite the huge responsibility they have had throughout their careers to shape the lives of their students.

Ken, A vast majority of teachers make a decent salary and if they invest a portion properly over the typical career of 25 to 30 years and and with receiving a pension should not be living in property.

I’ve read too many articles about teachers making BAD choices when it comes to investing. I provide these two as an example of teachers being “schooled”: http://tonyisola.com/2013/10/403beware/; http://tonyisola.com/2014/11/403beware-2/

As I have seen more and more hard working teachers cheated out of having reasonably-priced investments in their 403b plans, there are many who I have lost respect for along the way. Clearly, the best weapon for teachers is to get educated. Most teachers need to go back to school to relearn everything they have been taught about their so-called TDAs, and then they can demand the respect they deserve.

Ken, A vast majority of teachers make a decent salary and if they invest a portion properly over the typical career of 25 to 30 years and and with receiving a pension should not be living in property.

I’ve read too many articles about teachers making BAD choices when it comes to investing. I provide these two as an example of teachers being “schooled”: http://tonyisola.com/2013/10/403beware/; http://tonyisola.com/2014/11/403beware-2/

As I have seen more and more hard working teachers cheated out of having reasonably-priced investments in their 403b plans, there are many who I have lost respect for along the way. Clearly, the best weapon for teachers is to get educated. Most teachers need to go back to school to relearn everything they have been taught about their so-called TDAs, and then they can demand the respect they deserve.

Brian– Your mom was lucky that your dad got a MILITARY & CIVIL SERVICE pension–which as you are now glaring aware of, are GOVERNMENTAL benefits, and much higher than the average person’s pension.

The paper considers making retroactive changes in Social Security to address inadequate regulation of tax assisted retirement income.

Canada addressed this issue back in 1981 by making last survivor pensions the default option for all tax assisted retirement savings plans (unless the spouse had independent legal counsel to otherwise advise).

This one move dropped poverty among unattached female retirees dramatically.

Ontario also provides “free” medicine to retireds with only a dispensing fee.

The paper does not propose addressing the underlying causes of poverty among the elderly (lack of survivor pensions and high cost of drugs for the elderly) but, instead, proposes a “gift” from the OASDI – a Social Security plan with its own serious solvency problems.

Robin Hood robbed from the rich to help the poor. In this case, the OASDI is not “rich”.

The real problem is the $3.2 trillion spent a year on health care in the U.S. and at 18-19% of GDP; we spend 2x what European countries spend with no better outcomes. Most countries in Europe spend 7-9% and also have the same life expectancy as us.

Let us just ask for voluntary contributions to go towards a pool of money to help. It is not the governments responsibility to take care of the elderly, life is what it is. Military people earned what they got, same as anyone else who was promised something. Owed nothing more and nothing less.

I am disgusted and astounded by the righteous tone, ignorance and lack of caring demonstrated by Brian and others more concerned about other people’s personal choices than making sure American elderly can live out their lives in dignity with the care they may need. Well educated, intelligent people who live in stable situations can easily make wise choices. Too many of our citizens do not have the option as they struggle to survive from their earliest days or after crises they had no hand in creating. And Elizabeth Warren and Barak Obama were right when they reminded financially successful individuals that we all paid for the roads, police, military and educational services their business success depends on. As well as paying their pensions.

I believe that a more effective solution would be to eliminate income tax for everyone after age 70 regardless of income. Some high-tax states are considering this idea for property taxes, and the models show some surprising results that have implications for income taxation.

This is certainly a complex issue and not one with a simple straight forward resolution. Thanks for sharing this information and it’s helpful to have for anyone (at whatever point they start retirement planning) to consider.