Gen-X, Millennials: Now is the Time

Generation X and millennials, there is time.

Generation X and millennials, there is time.

In contrast to baby boomers, who are now mostly too old to rack up appreciable increases in their 401(k)s – though they should try – younger Gen-X and millennials have time and compounding investment returns on their side.

This blog examines how they are faring – millennials, because saving and investing well now poises them for a secure retirement, and Gen-X because this “ignored” generation is sandwiched between the financial demands of parenting and parent care. Their own assessments of their retirement preparedness appeared in a recent report by the nonprofit Transamerica Center for Retirement Studies (TCRS).

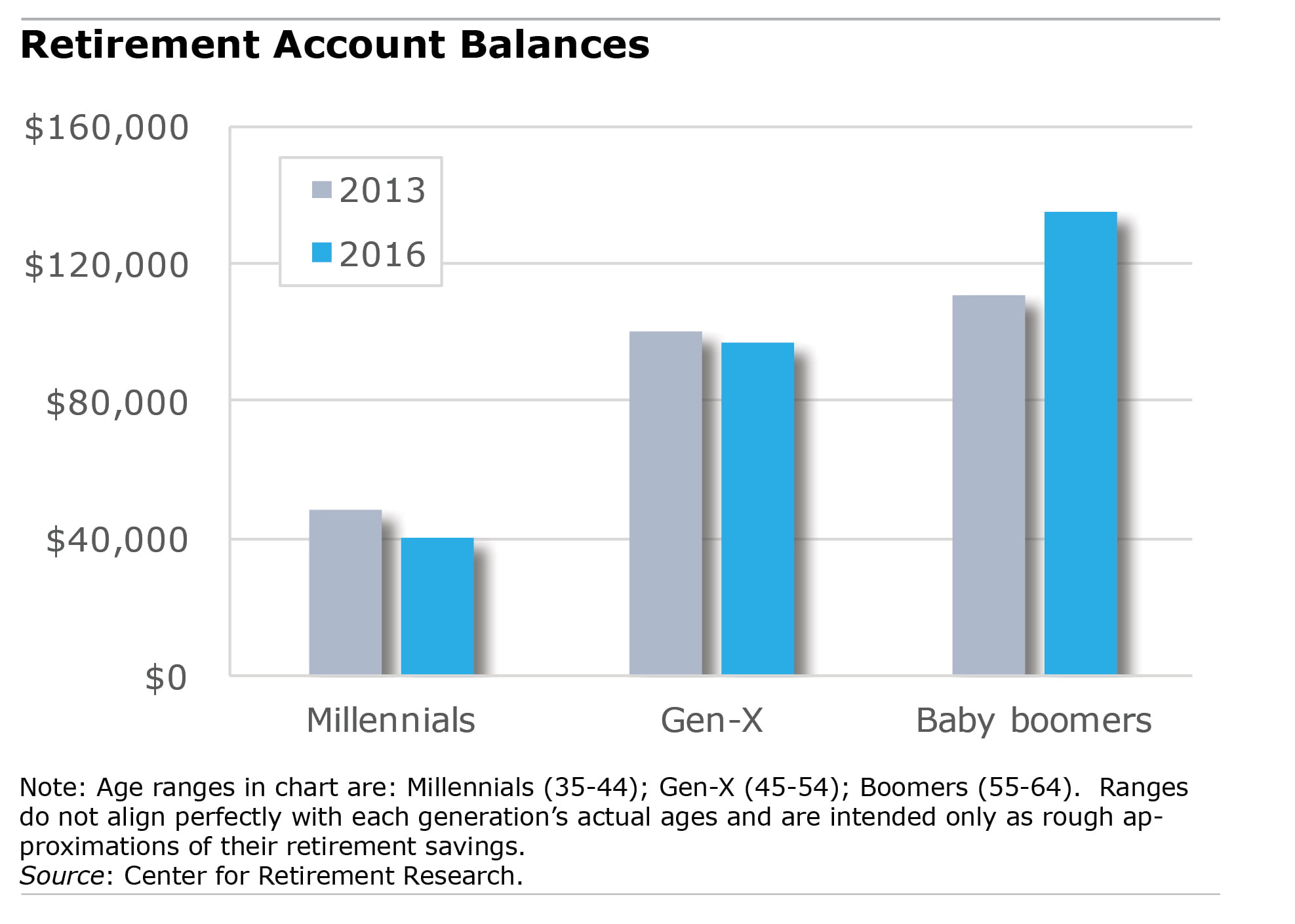

Millennials

“Millennials have heard the word that they need to save for retirement,” TCRS declared in its report summarizing its 2016 online survey of more than 4,000 workers.

Millennials’ ages are up through 37 in this survey. Nearly three out of four who have 401(k)s at work are already saving for retirement. They typically started saving at 22, indicating impressive foresight about retirement dates far in the future. Gen-X, ranging in age from 38 through 51, didn’t get started in earnest until they were 28.

While it’s great that millennials are saving for retirement, women in particular are not saving enough, said Catherine Collinson, president of TCRS. Among workers who participate in their employer’s 401(k) or similar plan, the survey finds that the typical millennial woman contributes only 5 percent to her plan, compared with 10 percent for millennial men.

Millennials aren’t taking advantage of their uniquely long investment time horizon, the survey finds. Retirement experts encourage younger adults to more aggressively invest 401(k)s in the stock market to enjoy decades of the long-term growth and compounding investment returns and potentially ride out the market’s inevitable volatility. Theoretically, if the stock market’s history proves true, equity-investing millennials can build up substantial retirement accounts, accumulating employers’ contributions and their own contributions and investment earnings over time.

But many millennials came of age during the 2008 financial crisis and still seem to be “in a state of shock with their concerns about the stock market,” Collinson said. One in five millennials say they are investing conservatively in bonds, money market funds, and cash.

Generation-X

Baby boomers will be the last generation with substantial access to traditional pensions. Gen-X is the first generation to heavily rely on defined-contribution accounts.

Only 12 percent of Gen-Xers feel they are saving enough, TCRS’ survey found. Behind this financial insecurity is a $97,000 account balance for the typical Gen-X worker, according to an analysis by the Center for Retirement Research (CRR) of combined 401(k) and IRA balances in the latest Federal Reserve’s Survey of Consumer Finances.

Gen-X retirement balances have shrunk $3,000 since 2013 – contrast that to baby boomers, whose balances have risen with the stock market since then. One potential explanation of Gen-X’s lost ground is a neglect of their investments at a crucial point in their working lives.

Forty percent said in the TCRS survey findings, “I prefer not to think about or concern myself with retirement investing until I get closer to my retirement date.” Ideally, 401(k) investments should be set and forgotten, but it’s advisable to check in on the fees charged by your mutual funds, to rebalance the portfolio periodically, or to consider a newly introduced target date fund, which would automatically adjust the investment risk for the worker as he ages.

But it’s also reasonable to speculate that financial pressures are bearing down on them from raising a family, sending kids to college, and sometimes dealing with aging parents. Gen-Xers are just as likely to care for an adult – their parents – as are aging boomers, who are usually their spouse’s first choice of a caregiver.

Evidence of Gen-Xers’ financial distress: 30 percent said they have borrowed or taken out early withdrawals from their retirement plans, TCRS found. This is slightly higher than baby boomers and considerably more than millennials, who have saved $40,000 so far.

Gen-X seems realistic about the upshot of their decisions: more than half said they either won’t retire until after 65 or do not plan to retire at all. Still, many of them view retirement as their top financial priority.

Gen-Xers’ and millennials’ retirement preparedness could use some improvement. But the important point is, now is the time.

Squared Away writer Kim Blanton invites you to follow us on Twitter @SquaredAwayBC. To stay current on our blog, please join our free email list. You’ll receive just one email each week – with links to the two new posts for that week – when you sign up here.

Comments are closed.

“Gen-X seems realistic about the upshot of their decisions: more than half said they either won’t retire until after 65 or do not plan to retire at all.” Realistic in the sense that they appreciate that it may be difficult to retire comfortably before 65. In the sense that they honestly believe they’ll be able to work after 65 – let alone working until death? Maybe not so much.

Rational arguments are part of the solution. And then there’s this:

http://www.anderson.ucla.edu/faculty-and-research/anderson-review/decumulation